How I found a great company using Warren Buffett's investment style

What I learned from Warren Buffett's Stock Market investing style, and how I added my own personal twist to make it easier.

Highlights

- Buffett's investing checklist.

- Converting checklist into a metrics filter.

- A deeper dive into metrics.

- Making sense of financials.

- My SIMPLER checklist.

I’ll explain his investing style, how I adapted it to make it simpler and found a great company to buy.

The key features of Warren Buffett’s investing style can be summed up in two of my favourite quotes.

[My] favourite holding period is forever.

AND

The stock market is a device for transferring money from the impatient to the patient.

Warren Buffett likes to buy good companies when they are cheap and hold onto them forever.

DISCLAIMER: I’m only explaining *my* technique! This is not financial advice, I am not a financial advisor and don’t play one on the internet.

Warren Buffett's investing strategy

I delved deep into Warren Buffett’s basic investing style and I came up with the following checklist. The 7 criteria for finding a good company, it must have:

- 1. A simple business model.

- 2. A moat (or a unique competitive advantage).

- 3. A low debt level.

- 4. Make enough cash to pay off their debt.

- 5. They have a predictable cash flow.

- 6. Their share price is currently low.

- AND the most important to me:

- 7. They return a consistent dividend.

The Why

Why would I choose companies that return good dividends? Well if we want to buy and hold, dividends give us an ongoing return.

A personal example:

I have an older friend and he is an excellent example of how companies paying dividends can be a great investment. He worked his whole life as a low level tradesman in the same job.

He invested a portion of his spare cash into the company he worked for. This company generally returns a dividend. He is now retired and can live off those dividends.

His investing style was similar to Warren Buffett in two ways. He invested in a company that paid good dividends, and he never sold a share.

The how - A stock filter

Now I get to where the rubber meets the road. How did I convert Warren Buffett’s checklist into something I can use to find companies?

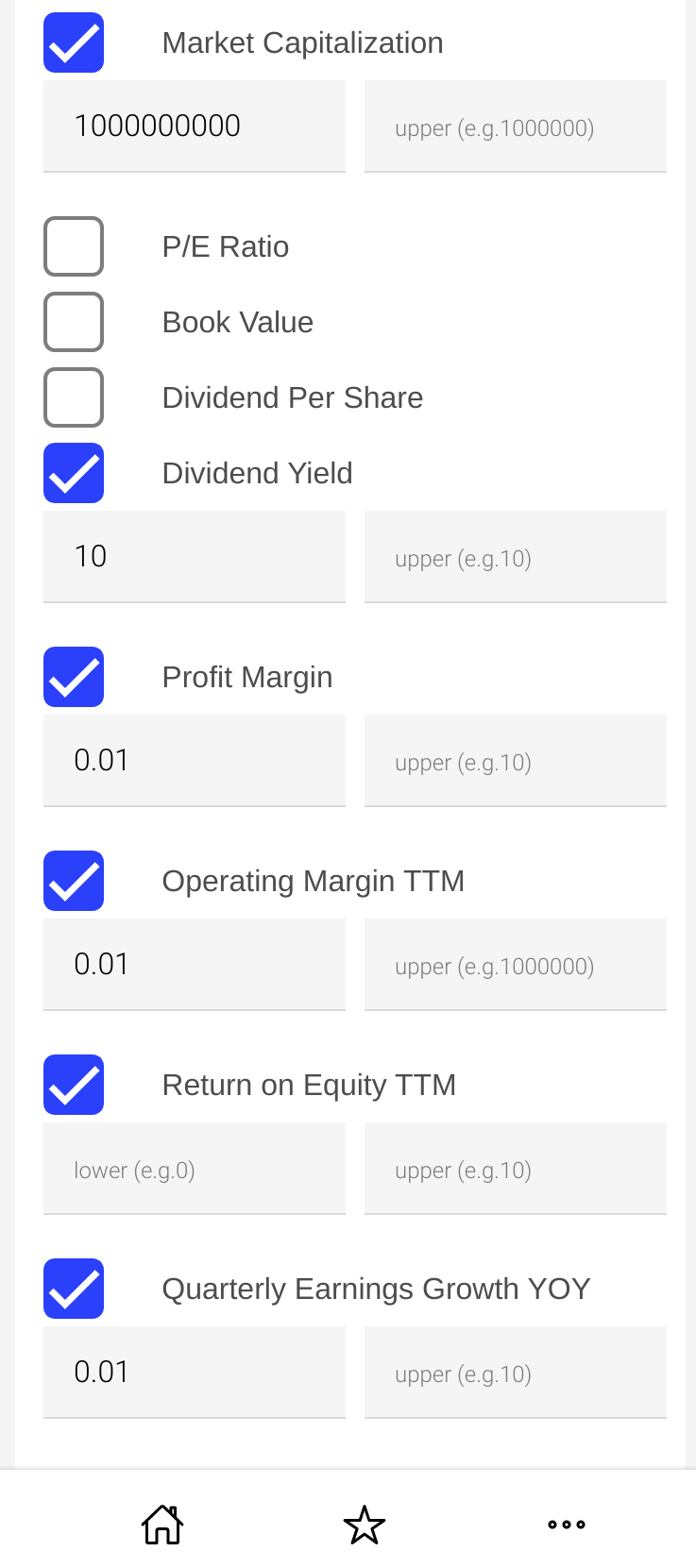

I used a stock filter!

With a filter I can sift through every company on a stock exchange. My filter returned companies that:

- Are mid-size or larger (Market Capitalization > $1B).

- Return a profit.

- Return a dividend of more than 10%.

Deeper dive into these metrics

Dividend Yield is the key figure I’m interested in. It gives me an idea of how much return I will get for my investment each year.

If I invest $1,000 and the Dividend Yield is 10%, I am getting $100 per year.

To make sure the companies are returning a profit I just need a positive value for Profit Margin, Operating Margin TTM and Quarterly Earnings Growth YOY.

Here is the filter:

Deep dive into each company

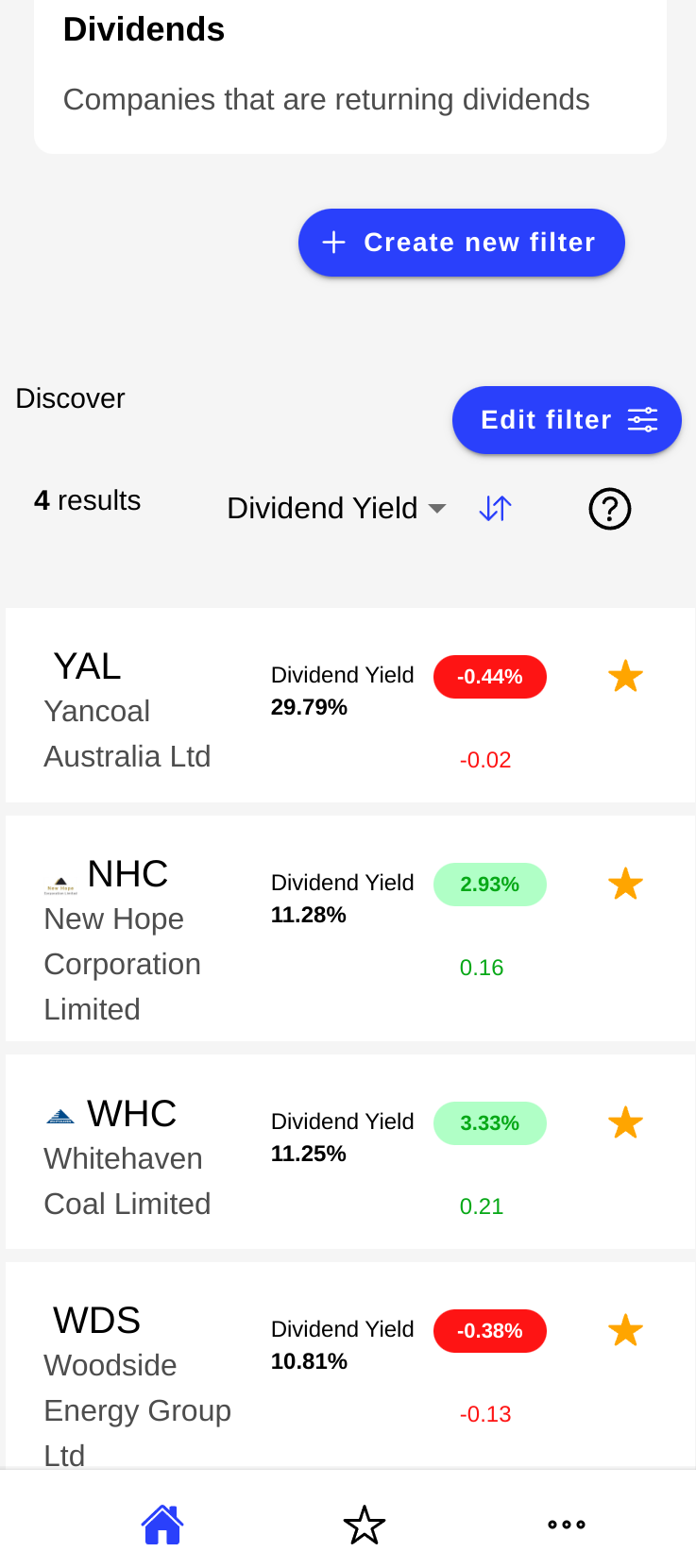

Using the filter above I got small list of companies to work with.

Next I had to examine each company in the list to rank them against Warren Buffett’s checklist. I’ll show you how I did that by using a company on the list, Yancoal.

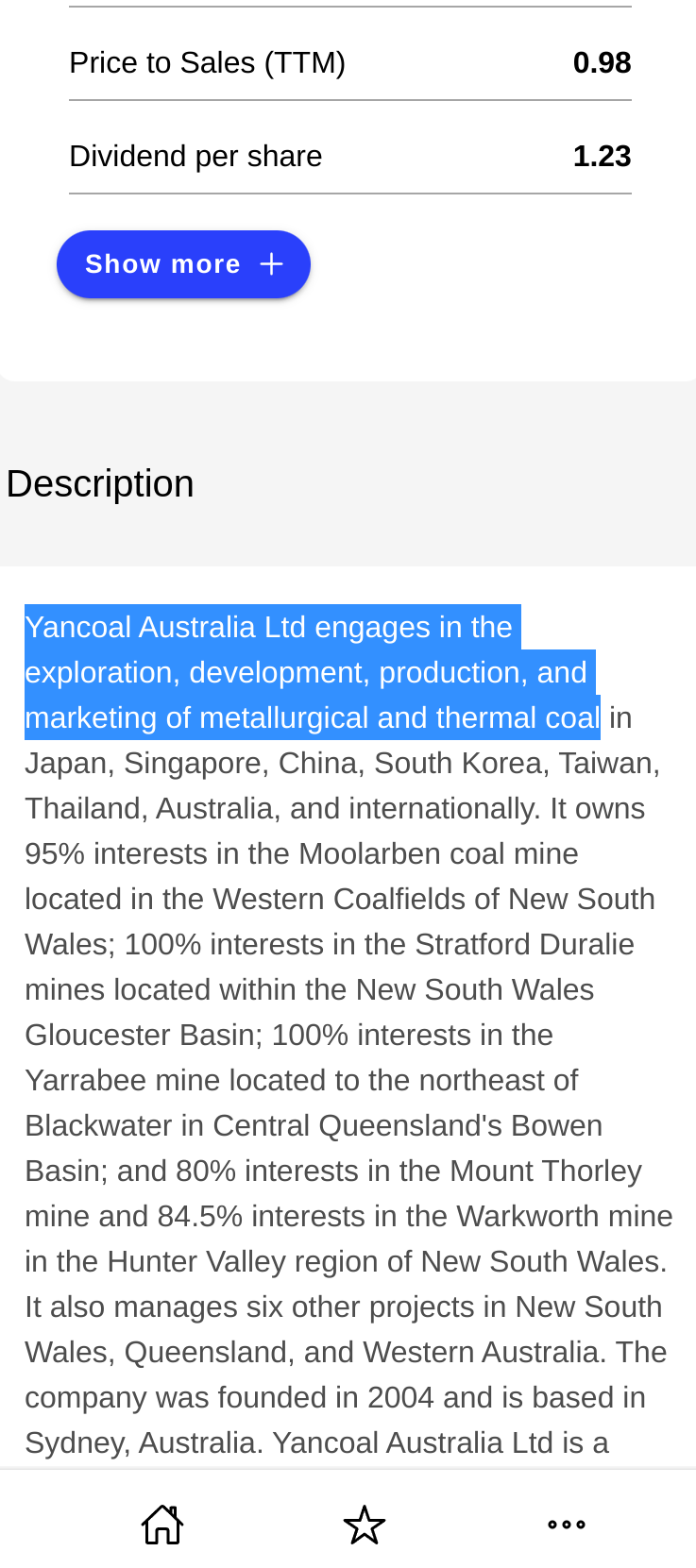

Simple business model:

This one is easy. Just take a look at their description and see if you understand what they do.

Yancoal explores, produces, develops and sells coal for making steel and energy. I understand the idea of coal in the production of steel and power, but I have no idea about all the variables that go into making a profit from it.

Do they have a simple business model? In my opinion that is a no.

Moat:

Does Yancoal have a moat (competitive advantage)? No. Australia alone is teaming with coal companies and there is nothing exclusive about the production of coal.

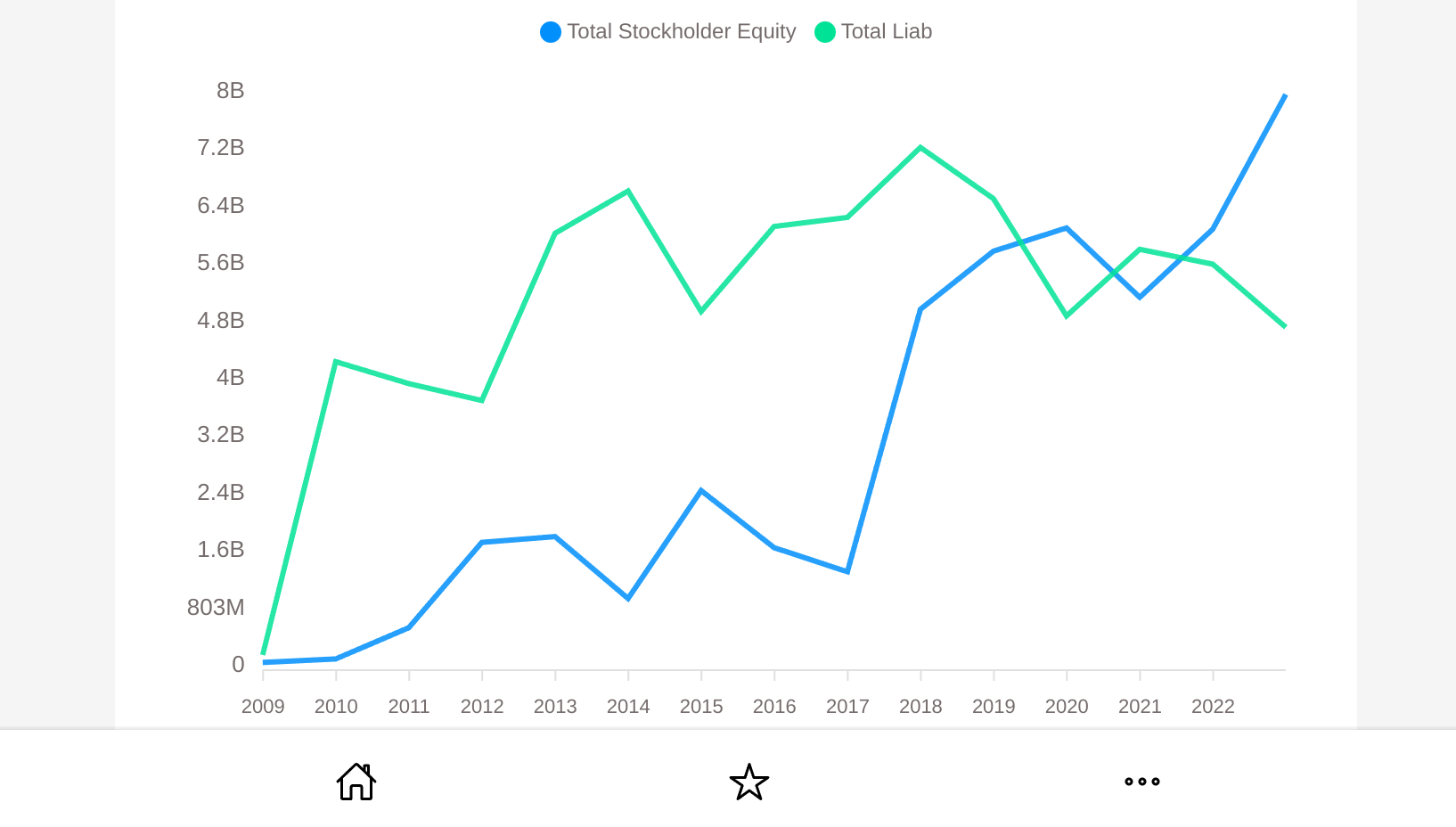

Debt to Equity:

Looking at total stockholder’s equity and comparing against total liabilities we can see it is not great. It is only in the last two years that it has looked good. That gets a 'no' from me.

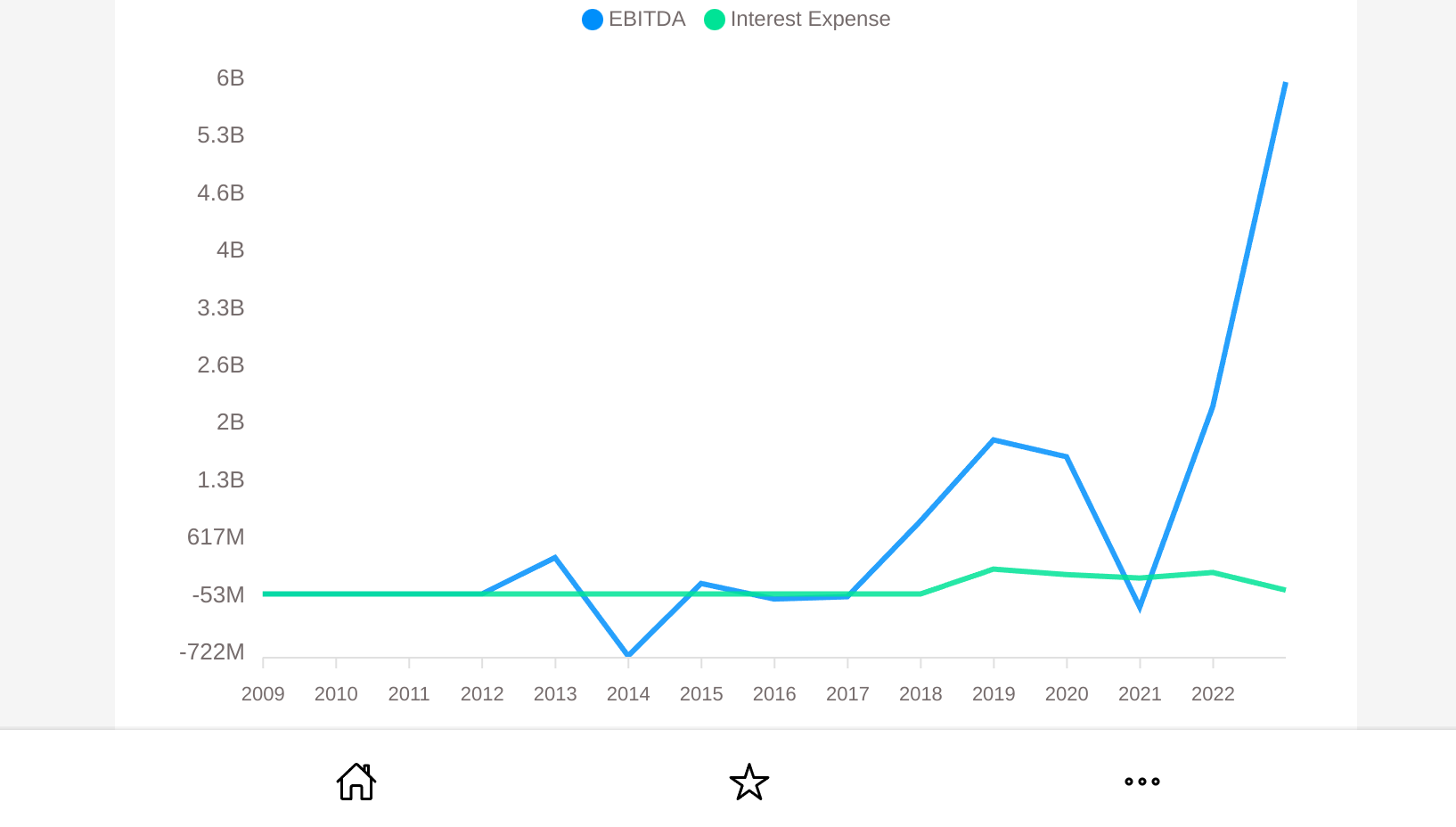

Interest Coverage Ratio:

Looking at earnings (EBITDA) and Interest expense we can see that earnings have only covered the interest on the debt for the last four years. Not promising. That gets a 'no' from me.

Low Debt Levels:

Another way to look at debt is to show total assets over total liabilities. Looking at this chart we see assets remain much greater than liabilities and have done so for a while, so that is a positive and gets a 'yes' from me.

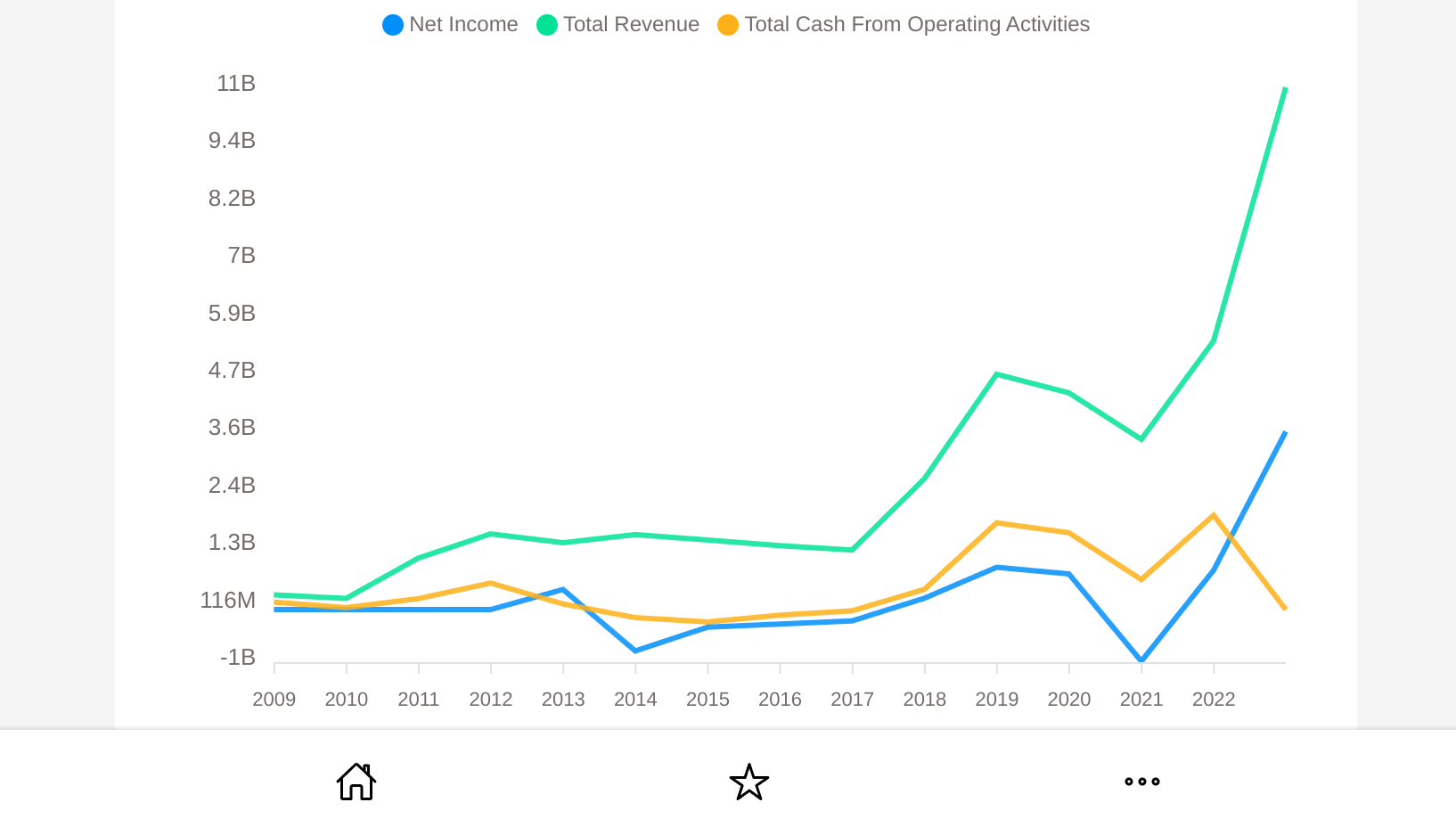

Predictable Cash Flow:

Let’s look at Net income, total revenue and total cash from operating activities. It looks steady recently but there has been a long period of losses, so I’m not happy with that and it gets a 'no'.

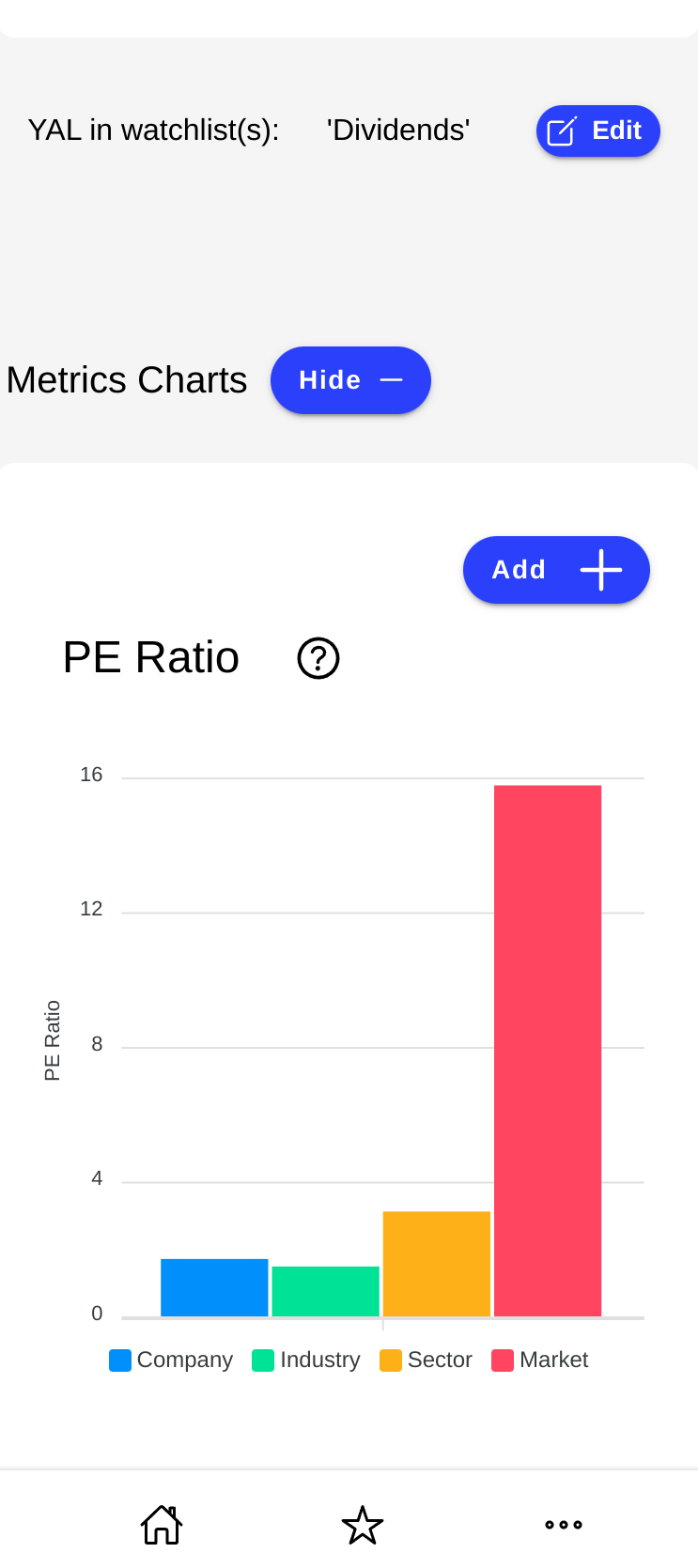

Price to Earnings:

With price to earnings it is more straightforward to compare. We can compare Yancoal’s price to earnings against its competitors by looking at the price to earnings bar chart. It does well compared to the industry, sector and the rest of the market.

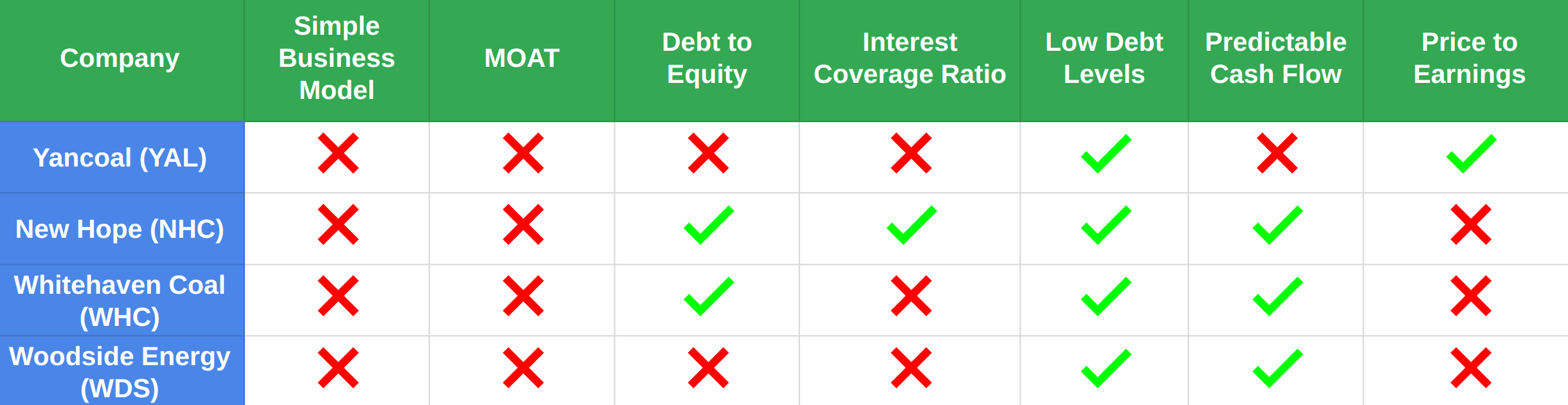

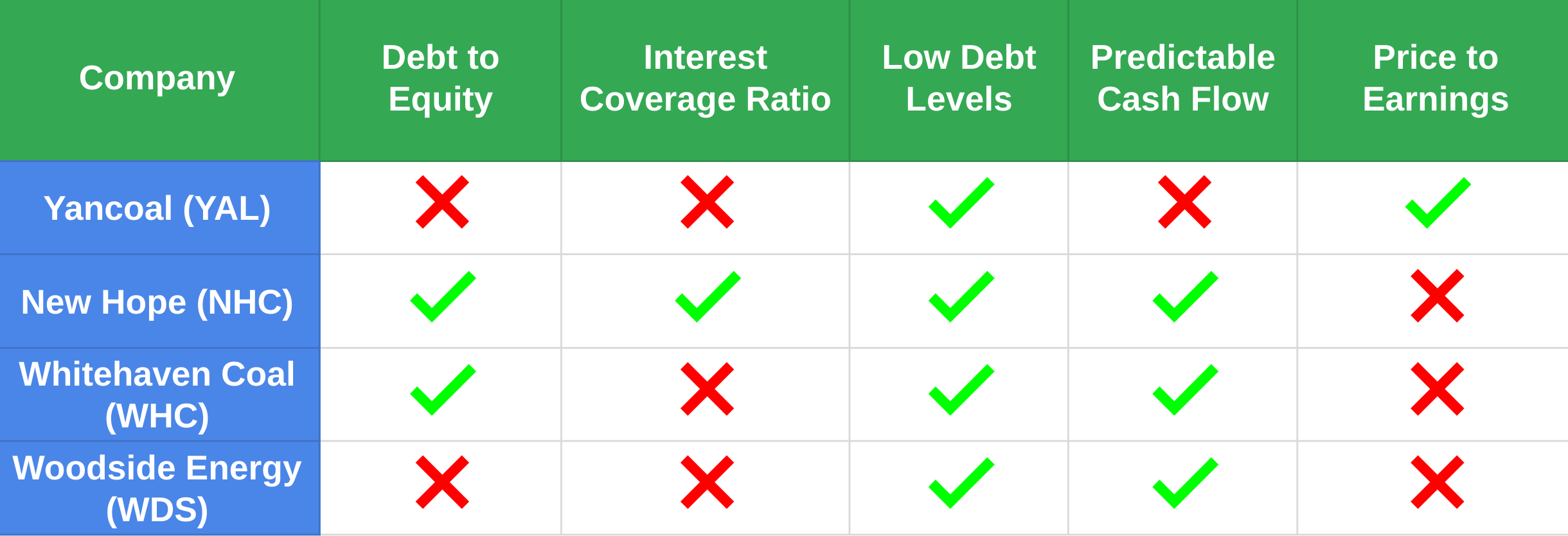

The results of all companies

Because we have a small list of companies it is not hard to go through and answer Warren Buffett’s checklist for each. And here is where I explain why I’ve adjusted the checklist, why it is simpler and why I think it still makes sense.

Here are the results from my investigation:

You can see in this list that no company has a ‘Simple Business Model’. And no company has a ‘moat’. And this is where my method differs from Warren Buffett.

Warren would not touch a company that he doesn't understand. He has famously missed investing in big tech companies, like Amazon and Google, because he did not understand their business well enough.

He also loves investing in companies with a moat, like Coke.

My simpler checklist

My checklist REMOVES two things: The need for a simple business model and a moat.

You might ask, who do you think you are removing those two requirements? Warren Buffett is the GOAT! And I’ll answer your question by saying. I HAVE to or I’ll never invest in any company!

Removing simple business model:

As for a simple business model. I can kind of understand the coal industry in CONCEPT, but I have no idea what all the variables are. Do I ever really understand a business? I understand some more than others, but if I say I understand a business am I just fooling myself?

I understand the tech sector a little because I work in it! But I wouldn't say I understand it very well.

Removing moat (competitive advantage):

And for a moat? What company truly has a moat? A very small number that I can think of, and most of those companies are in the tech sector. And companies in the tech sector are notoriously over-priced and are growth oriented, not dividend, oriented. So not great for long-term investing for dividend returns.

What did I buy?

What company did I end up buying? Well I decided to go with ‘New Hope’.

It ticked the most boxes.

It had a good debt to equity ratio, good interest coverage ratio, stable and predictable cash flow, decent dividends and the stock price was reasonable.

I have now bought some shares and we’ll be able to see how well it does over time.

I’ll leave you with that for now. I’ll try and keep more blogs/videos coming and pass on what I have learned about stock investing.

Recommended next article

Subscribe to EquiShark updates

If you enjoy reading our blog, sign up here and get email alerts when we release a new one.

We respect your privacy and will keep your email private. Unsubscribe at any time.